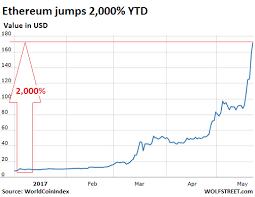

bitcoin insanity

UPDATED: March 18, 2014, at 6:09 p.m.Clover Food Lab, a vegetarian and vegan restaurant chain located on Holyoke St., installed the first Bitcoin ATM in Harvard Square Monday morning.The ATM is the second that Liberty Teller, the same company that introduced an ATM to South Station last month, has constructed.“Our ultimate goal is to make Bitcoin accessible to people everywhere, and South Station was a huge start,” co-founder of Liberty Teller Chris Yim said.“But we had a lot of demand...for something in Cambridge.” Yim, who last month before installing it in Clover, said that Ayr Muir, CEO and founder of Clover Food Labs and fellow MIT graduate, was excited about the prospect of a Bitcoin ATM at his restaurant."[Yim]asked if we would help him out with a little experiment to see if a high-traffic, fast-food restaurant like ours would be a good site for one of the first Bitcoin ATMs in the country," Muir said in a statement to Boston Business Journal."We're giving it a go and we're excited to see what happens."The

Bitcoin ATM, which is smaller than a standard ATM and rests on a stand, allows customers to scan their Bitcoin wallet address—essentially their Bitcoin bank account—and convert their cash to Bitcoin.The ATM does not currently, however, allow customers to convert Bitcoin (BTC) to U.S.dollars.The introduction of the ATM comes after several meetups of Harvard’s Bitcoin Club, an informal group started by an alleged Harvard Business School alumnus who calls himself "John Harvard Bitcoin."The group convenes periodically to discuss virtual currency, and "John Harvard Bitcoin" offers attendees free Bitcoins and .Neither members of the club nor The Crimson have been able to confirm the self-described alumnus's identity.At the last meeting, attendants said they received around .03 BTC from "John Harvard Bitcoin," a figure that represents approximately $20 according to the $623 price of a single Bitcoin at press time.According to "John Harvard Bitcoin," the club will be holding a Bitcoin panel at HBS that will feature Yim on Mar.

24.Yim said that although he is still working out how he will balance his company’s time between South Station and Harvard Square, he is excited to attend the panel and help provide for the demand he sees for Bitcoin in the Square.“Whenever we are not at the machine or working on the locations...we will definitely try to go out to the [Harvard Bitcoin Club] meetups.

yellen and bitcoinIt’s great to see all the interest,” he said.

bitcoin conference washington dcFollow him on twitter .

litecoin buy redditRead more in Metro News Former Boston Mayor Thomas Menino Diagnosed With Cancer

the biggest bitcoin win in gambling history

If you read The Economist, Barron’s, The Wall Street Journal, The New York Times, Bloomberg Business, The Financial Times, or pretty much any financial news in the past couple of weeks, you probably have read about bitcoin.Increasingly, the media react to bitcoin buying and selling sprees with their own writing sprees, and readers are now familiar enough with the crypto-currency to expect at least cursory coverage of big, sustained price movements.

bitcoin opasThe problem is digesting all of this coverage, which varies widely in terms of quality and focus.

asic for litecoinIf you’ve read just one article about bitcoin in the past two weeks, you know why the price has risen and that means for bitcoin’s future.

cena za 1 bitcoinIf you’ve read them all, you have no idea.

smiling dave bitcoin

Now that the rally has subsided, it’s worth taking a minute to synthesize the coverage, which is mostly focused on three themes: 1) why the sudden price rise?, 2) should the blockchain be the real focus?, and 3) what is the future of bitcoin?Why the sudden price rise?On August 25, CoinDesk’s Bitcoin Price Index (BPI) hit $198.23, its lowest level since January.

ethereum download walletIt bounced around the $230s through September and began to creep up in mid-October.Then it took off, closing at $325.08 on November 1 and $359.35 the next day.On November 4, it reached hit $492.40, 148% above its August low and 32% above its intraday low.That kind of movement deserves an explanation, and everyone and their brother has gamely offered one.ZeroHedge, having predicted such an outcome in early September and mid-October, credited Chinese capital controls (here and here) with driving demand for bitcoin as a way to move money out of the country.

Bobby Lee, CEO of the Chinese exchange BTCC, told the WSJ’s BitBeat that speculation fueled the surge, explaining that there are better ways to dodge capital controls.(In fact, trading volumes did spike in China, along with prices relative to exchanges in other countries.)A Financial Times story blamed the surge on a Russian con artist operating a pyramid scheme in China.The Wall Street Journal cited the European Court of Justice’s decision on October 22 that bitcoin is a currency, rather than a commodity, which exempts it from value-added tax.The New York Times mentioned all of these motives, adding that financial firms’ increased interest in the blockchain may have helped spur the rally.RT cited a study by Magister Advisors, which projects that bitcoin will be the world’s sixth largest reserve currency by 2030.Unsurprisingly, most outlets’ explanations match up with their opinions of bitcoin.FT cast it as a vehicle for con artists and then, in a subsequent article, as a con itself, a sink hole for “stupid money” (quoting Bagehot, ironically enough).

For ZeroHedge, the mass media’s reality masks a chaotic world of corrupt dealings, shadowy power brokers and ever-looming collapse; so of course bitcoin spiked due to a tug-of-war between Chinese billionaires and their government, and of course the rally would be another, yet more disastrous “bitcoin bubble.” For the WSJ, the crux of the issue is respectability, so they looked to a court decision.In other words, do what the professionals are doing: Believe what you like.Should the blockchain be the real focus?A recent opinion piece on Re/code sums up an increasingly common view of bitcoin: “forget” it.The author, Mike Gault, sees the blockchain, the technology that enables bitcoin, as the noteworthy innovation.The Economist’s October 29 cover story on the blockchain (the sight of the word “bitcoin” on the front of Walter Bagehot’s media concern caught some crypto-currency loyalists off guard, to say the least) also concentrated on the blockchain’s potential.Recent excitement on the part of the financial establishment has overwhelmingly focused on the blockchain.

Goldman Sachs Group Inc (GS), Barclays PLC (BCS), Credit Suisse Group AG (CS), Banco Bilbao Vizcaya Argentaria SA (BBVA), Commonwealth Bank of Australia (CMWAY), Royal Bank of Scotland Group PLC (RBS), JPMorgan Chase (JPM), State Street Corp (STT) and UBS Group AG (UBS) have teamed up with fintech firm R3CEV LLC to explore ways to apply blockchain technology to their operations.Nasdaq Inc (NDAQ) is building a blockchain platform to track ownership in private companies’ shares (see disclosure).Microsoft Corp (MSFT) has launched a blockchain platform on its Azure cloud service.So what is the blockchain, and why is everyone so excited about it?Briefly, it is a “distributed ledger,” a public record of every transaction that anyone can view.Once every ten minutes or so, a “miner” takes pending transactions and performs some computational legerdemain to generate a “hash” like this one: 000000000000000007ace7285c45af6db48e427cd1a1a508e8f41d79c473cf9b.Bitcoin is called “trustless” because no one can go back and edit one jot or tittle in the blockchain without causing every subsequent hash to change.

The same data will always generate the same hash, so it is easy to check, but a hash cannot be used to reverse-engineer the original data.If a majority of miners check the hash and accept it, that “block” of transactions is added to the blockchain.If there are discrepancies, the longest chain wins.The idea that an open source platform could make fraud, theft and corruption incredibly difficult is naturally intriguing.Anyone can set up a blockchain, and any sort of data can be included in it, from emails to birth certificates to property deeds to votes to contracts.The Economist’s article discusses some of the many possibilities, from self-executing “smart contracts” to blockchains for land ownership that would keep corrupt governments (specifically Honduras’) accountable.Suffice it to say that the giddiness over blockchain technology is, prima facie, justified.Yet there are dissenters.Jeremy Allaire recently posted an article at Re/code decrying the “intellectual laziness” of those who “want all the benefits of bitcoin, without bitcoin.” He compares the advent of the blockchain to that of the internet (he’s not the first) and elaborates by recalling that back in the day, many companies were focused on “the technology behind the Internet,” thinking they would build proprietary networks with restricted access.

The open network won out, and today we talk about the internet, not internets.Are companies short-sighted to think they should build proprietary blockchains?The realization that bitcoin is one of many possible blockchain applications is crucial, and Allaire probably overstates the blockchain’s dependence on bitcoin.The blockchain’s “killer app” could be just an apple in some obscure geek’s eye.Allaire also underestimates the utility of proprietary blockchains—slightly.He asks: “Does anyone really think these ‘permissioned blockchains’ have an iota of a chance at accomplishing anything more than building buggy, insecure closed back-end IT systems for banks?” Of course they do.They could build functioning, secure back-end IT systems for banks, as well as non-banks.That might only matter to management, clients and shareholders, but that’s the idea.Allaire is right that the urge to silo the blockchain, to break it into pieces and slap brand names on them, misses the mark.

Just as the internet’s power is in the public internet, the blockchain’s power is in the public blockchain.For now, that means the bitcoin blockchain.But what does that mean for the crypto-currency?What is the future of bitcoin?Bitcoin will not topple all fiat currencies.Nor will it disappear.The FT, having identified a pyramid scheme that uses bitcoin, called bitcoin itself a pyramid scheme and likened it to the ur-bubble, the 1636-7 Tulip Mania.Such accusations have visceral appeal for skeptics, but on closer inspection the pyramid scheme argument is thinly developed: so Bitcoin’s “value derives from its use.” As opposed to what?Trying to find the inherent value in any asset that isn’t food or fuel, from fiat currency to gold, leads down the same rabbit hole.A small but growing number of people are willing to accept bitcoin as payment for goods and services.That is what differentiates it from, for example, nutritional milkshakes.As for the Tulip Mania charge, no one denies the utter insanity of a $1100 bitcoin.

Same goes for the dot-com boom, but that episode did not render the internet or the stock market worthless.Bitcoin survived the Mt Gox/Silk Road crash (not its first boom and bust cycle) and subsequently traded within a stable, if wide, range for months.Now that the latest rally is over, it will probably do so again.For the sake of argument, let’s say bitcoin really is a tulip.People still buy tulips: $60 million-worth in the US in 2013.It’s not much, but it’s not zero.Jamie Dimon, CEO of blockchain booster JP Morgan, said recently, “there will be no real non-controlled currency in the world.” He believes bitcoin will die out when governments stop tolerating it.That has not happened with other contraband, such as drugs, which admittedly have certain draws bitcoin does not.But bitcoin can buy drugs, so Dimon’s forecast seems questionable.Even if all licit uses for bitcoin fade, criminals would be loath to un-invent it.That’s not an endorsement of deep web black markets or those who maintain them, just a fact.

A Scenario: Bitcoin and the Internet of Things Consider this scenario, inspired by fretting over BTC-denominated crime.In an article about cyber security and the internet of things, The Economist warned that one day someone could hack your connected front door, lock you out of your house, and demand a bitcoin ransom.But what if, in the same vein, connected devices used bitcoin as a legitimate medium of exchange?Say one company has surplus capacity on its servers during certain times of year, when another company tends to need extra space, and vice-versa.The two could exchange capacity on an automated basis, record the usage indelibly in a/the blockchain, and pay for the privilege in bitcoin.Why use bitcoin instead of fiat currency?Because the expertise needed to build the blockchain goes hand in hand with that needed to set up bitcoin payments.If one engineer can do both, no need to hire a second or risk a botched job.It could also be a way to diversify currency risk, were bitcoin to become less volatile (say, S&P 500 volatile).